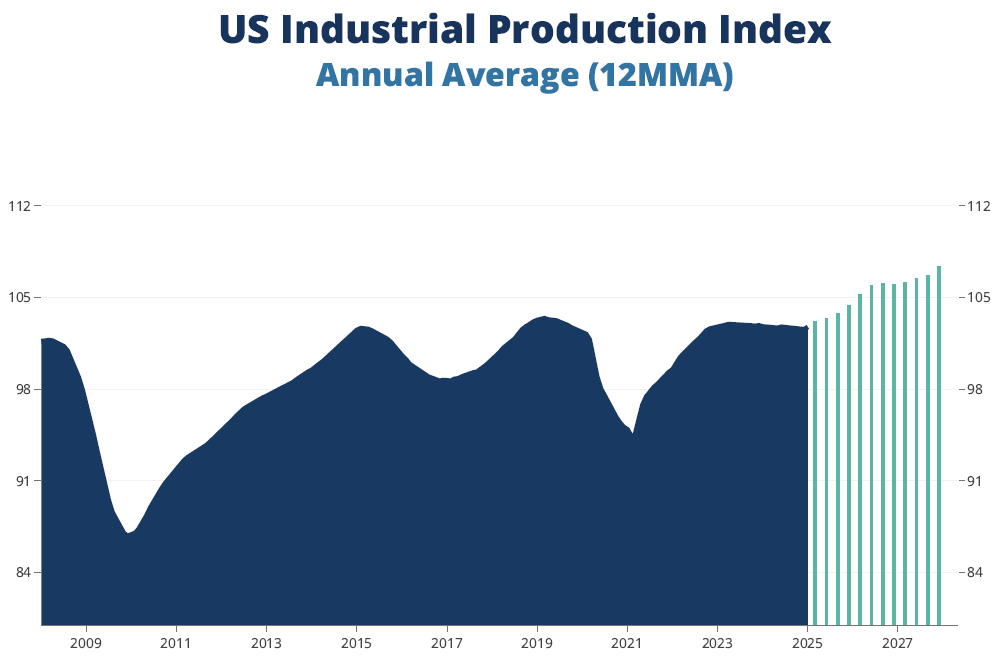

Tariffs, geopolitical conflict, interest rates, inflation, stock market volatility, and more are on the minds of businesses and consumers, leading to elevated uncertainty. As we parse the various headwinds and tail winds, we are maintaining our outlook for macroeconomic growth in the coming years. A number of leading indicators, including rise in the US Total Industry Capacity Utilization Rate and ITR Leading Indicator™ signal that there will be rise in 2025 and into at least 2026. However, in general, 2025 and 2026 will be muted relative to the prior cycle, and we want to emphasize that underneath the headline numbers, there are divergent outcomes. Knowing your market’s trends is key.

Rising real incomes, as well as our expectations for generally rising consumer prices, suggest that Retail Sales will rise in the coming years. Not all consumer demographics are performing the same though – a large portion of consumer expenditures are made by high-income brackets . If your business caters to lower-income brackets, who on net are struggling to build up savings as prices generally rise and long-term interest rates stay sticky, your sales may not trend as closely this cycle with broader Retail Sales. Consider who your target demographics are when making business decisions.

Businesses are also in a stable position with elevated corporate profits, and business confidence metrics are slowly rising. US Nondefense Capital Goods New Orders, a proxy for B2B spending, is tentatively rising and poised for further rise in the rest of 2025 and throughout at least 2026, though growth will be muted relative to recent cycles. Businesses are contending with still-elevated borrowing costs, which will limit some capex. However, we urge clients to avoid trying to time a low for borrowing costs and instead invest in new capacity whenever it would most benefit their business. Our long-range expectation is for interest rates and inflation to generally rise given the multitude of inflationary drivers present in this cycle.

Construction trends differ from the macroeconomy and much of the industrial sector. The residential sector, which leads the macroeconomy, is undergoing very mild decline due in part to persistent affordability constraints. While these constraints are likely to persist, mild rise is on the horizon for US Single-Unit Housing Starts given the underlying demand for more housing. Multi-Unit Housing is facing other challenges and is likely to stay well below the stimulus and low-interest-rate-fueled 2022 level of activity. This is due to current interest rate headwinds and greater financial strains for those on the lower or middle end of the income spectrum, who predominantly rent multi-unit housing. The nonresidential construction sector, which lags the macroeconomy, will generally decline mildly this year and next due in part to elevated interest rates. However, be prepared for shifts within the overall nonresidential sector, with some segments of institutional construction, like education, lagging overall nonresidential outperforming and others that have been outperforming, like manufacturing, facing the impact of government incentives wearing off.

Tariffs are at the forefront of the minds of businesses and consumers alike. At ITR Economics, we are apolitical and analyze policy solely due to its economic implications. Tariffs create winners and losers in the marketplace; some will face pain, while others will benefit from the shift in the competitive landscape. Where does your business fall within this spectrum? Consider your direct exposure to tariffs and the upstream and downstream effects on your business.

While each business’s situation is unique, there are some recommendations we think apply broadly. The first is to focus on efficiency: Pricing pressures will increase in the coming years for both inputs and labor, which could cut into profits. Second, if you plan to finance business investments, focus more on the payback period rather than trying to time a low in interest rates, as they are likely to remain sticky. Our third recommendation is that you factor a challenging 2030s cyclical downturn into your longer-term plans. There is still time to position your business and personal finances to prepare for those tougher times, but the runway is rapidly shortening. Stagnation is terminal – growth requires constant attention and change.