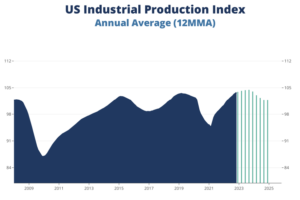

Rain or shine, we constantly monitor our system of leading indicators for signs of improvement or deterioration. In the last quarter, we’ve seen broad-based weakness, coupled with a new signal: short term interest rates – as measured by 3-month treasuries – are now higher than long-term interest rates, as measured by 10-year treasuries. This so-called “inverted yield curve” is a signal that there is an 88% probability of a US Industrial Production recession coming, as the Federal Reserve has raised short-term interest rates too far, too fast. But three main tailwinds will keep the recession relatively mild.

We lowered our annual average US Industrial Production forecast downward by a slim 0.4% for 2023. Instead of the mild growth (+1.6%) previously forecast, we now expect activity to be virtually flat for 2023 (+0.1%) relative to 2022, with decline developing late in the year. 2024 is impacted more significantly. Prior to the extremely sharp and fast rate hikes by the Fed, we were expecting growth for 2024. Now we expect decline to extend throughout 2024, with 2024 coming in 2.3% below the 2023 average, as it typically takes just over a year for yield-curve inversions to translate into a recession.

At the bottom of the cycle in 3Q24, we are calling for 2.6% year-over-year contraction. We’ve experienced a similar severity of decline in US Industrial Production three times in the last 30 or so years: the early 1990s macroeconomic recession, the early 2000s macroeconomic recession, and the 2015-16 recession. The 2015-16 recession only impacted the industrial sector and was particularly unrelenting for companies tied to oil prices. Expect this cycle to be more like the early 1990s or early 2000s.

Three main tailwinds – reshoring, backlogs, and a solid consumer balance sheet – will keep the recession relatively mild. Companies continue to be interested in positioning their supply chain closer to the North American consumer base, and backlogs will continue to be worked through as the supply chain loosens. Meanwhile, our examination of consumer balance sheets revealed that the aggregate consumer debt-to-income ratio, particularly the credit card debt-to-income ratio, is in a healthy place. Simply put, consumers are not overleveraged, which is the opposite situation that the US economy found itself in going into the Great Recession.

It will be especially important to understand the degree to which your business will (or will not) be impacted by a macroeconomic recession. Use the forecasts in this report to help. In general, industries that benefitted greatly from stimulus in 2020-21 (outdoor equipment, single-family housing in expensive areas, etc.) are most at risk of a pullback in 2023-24. In addition, discretionary markets like tech are likely to underperform essentials in the food industry, healthcare, and utilities, as consumers will prioritize deploying tighter dollars to where they are most needed. Meanwhile, there will be some loosening in the labor market – though not marked, given demographics – particularly in 2024. Take this as an opportunity to upgrade your talent pool in preparation for recovery and rise starting in 2025.

There are an elevated number of risks to our forecast both to the upside and to the downside because of domestic and international political events at play in this cycle. The degree of monetary and fiscal stimulus that was deployed in 2020-21, and is now being withdrawn, is unprecedented. The war in Ukraine and general nationalist/protectionist sentiment around the world, coupled with a pandemic, only adds to the uncertainty. In spite of this, the labor market and consumer balance sheets look very strong, offering upside risk.

What can you do amid the uncertainty? First and foremost, make a plan and work the plan. Determine what impacts the recession will have on your business (reach out to us if you need help). After making those determinations, put baseline budgets and strategies in place to maximize your competitive advantages in the recessionary landscape. Get your employees excited and focused on implementing those strategies, but don’t stop there. We will regularly be in contact with our clients and providing updates if the upside or downside risk factors lead us to change our baseline forecasts. You should have plans at the ready to adjust as things develop. Monitor your cash flow more carefully than before. Lastly, lead with confidence and be opportunistic. Your competitors may go into panic mode. Don’t follow them there.